Tenant Buyouts

I do not charge contingency fees based upon a percentage of the buyout amount. I only charge for the time I spend to negotiate, correspond, draft, review and finalize the agreement, resulting in substantial savings for our clients.

I also review agreements that tenants have negotiated for themselves. I often revise those contracts to include non-material terms to strengthen enforcement for the benefit of the tenant. Generally I find that I can charge a flat rate for an hour of my time to review, revise and to answer all of your questions.

Rent Ordinance section 37.9E governs tenant buyouts.

In an effort to 1) increase the fairness of buyout negotiations by requiring landlords to provide a statement of the rights of a tenant; to create a right of rescission for tenants; 2) to allow a tenants time to consult a tenant’s rights specialist; and 3) to collect tenant buyout data, the San Francisco Board of Supervisors passed Rents Ordinance § 37.9E to regulate tenant buyouts in March 2015.

The Rent Board created a Pre-Buyout Disclosure Form that the landlord must submit to the tenant before engaging in negotiating a buyout. The landlord must file the form with the Rent Board along with a Declaration of Landlord Regarding Service of Pre-Buyout Negotiations Disclosure Form. If the landlord and tenant agree to a buyout, the landlord must file the agreement with the Rent Board within 46 and 59 days from the execution of the agreement. All agreements must be in writing. The tenant has 45 days to rescind the agreement. The Rent Board will post all buyout agreements in a searchable database, available to the public.

What do I do if I receive a pre-buyout disclosure form?

I receive many calls from tenants who have received these forms. You really don’t have to do anything if you receive the form—you can toss it, use it as scratch paper or wad it into a ball as a cat toy—but that wouldn’t be my advice.

Even if you haven’t received a pre-buyout disclosure along with a lawyer’s “win-win” letter (a letter containing a threat that the landlord will move into your unit despite the fact that that he’s a pineapple grower who lives in Hawaii or an Ellis Act eviction threat), you must still treat service of the disclosure as an implicit threat.

My advice would be to sign the form and send it back to the landlord. Signing a pre-buyout disclosure form does not obligate you to negotiate a deal or even to take a deal you negotiated. Signing this form doesn’t obligate you to anything. But signing the form does give you an opportunity to engage with the landlord to get more information. As I stated in my article Buyouts, it’s very important that you get as much information about the landlord to understand his real intentions.

Calculate your absolute bottom line for tenant buyouts.

My article, Tenant Buyouts: Your Absolute Bottom Line is as appropriate today as when it was written in 2010. I recently updated the statutory relocation payment amounts to demonstrate how to figure your bottom line. In the article, I asked you to evaluate your household’s absolute bottom line by looking at the statutory relocation payment based upon the number of tenants in the unit, their ages and their disabilities. I also point out that you should always include your security deposit and accrued interest in your bottom line. To calculate your interest see the San Francisco Security Deposit Interest Calculator on this page.

You should never take a buyout for less than what you could get if the landlord follows though on his or her threat to evict.

Sadly though, one can can peruse some of the latest tenant buyouts data and find many tenants who accepted buyouts worth less than the statutory minimum relocation payments.

Some landlord attorneys recommend that landlords only offer a buyout based upon the average buyout in a given neighborhood or even based upon citywide statistics, The number of uninformed tenants bamboozled into taking less than statutory relocation payments significantly lowers the average buyout price.

Do the math—location, location, location!

In Tenant Buyouts: Strategy for Success, I discussed the fact that you’re probably not going to get a down payment for house in San Francisco from a buyout—not that it shouldn’t be required by law—but that it’s unlikely. I also discussed the (now diminished) ramifications of Subdivision Code § 1396.2 (multiple evictions and evictions of disabled tenants and elderly tenants as a bar to condominium conversion.) I also provided some techniques for negotiation, including gathering information, allying with other tenants in the building and assessing the landlord’s true intentions.

Here, I want to show you exactly how much a given building will increase in value if the landlord can buy out only out one tenant. Let’s do the math.

Calculate the building’s increased value if you vacate by using a capitalization rate.

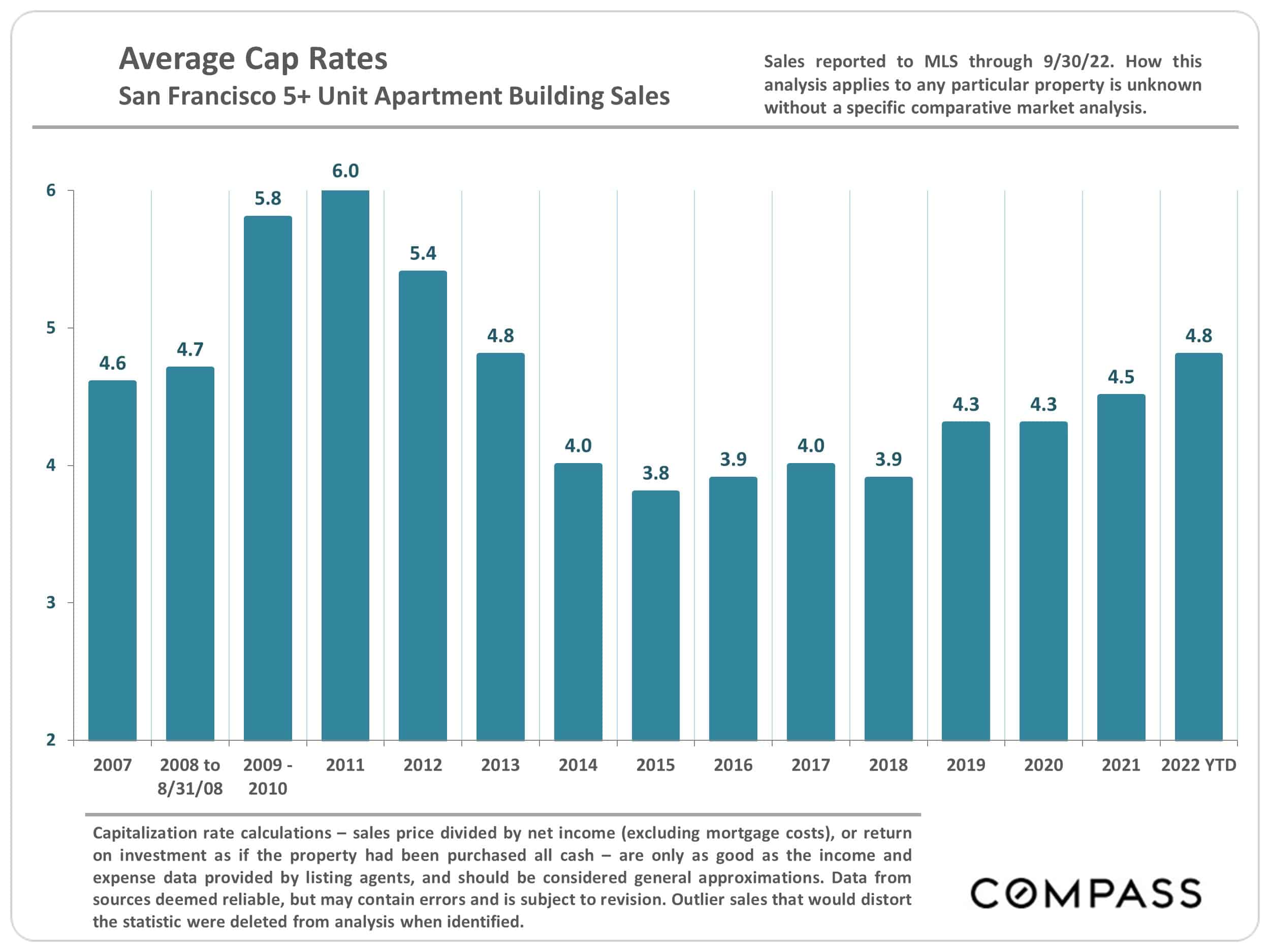

What is a capitalization rate? The capitalization rate, often just called the cap rate, is the ratio of Net Operating Income (NOI) to the property’s asset value. So, for example, if a property recently sold for $1,000,000 and had an NOI of $100,000, then the cap rate would be $100,000/$1,000,000, or 10%.

If you already know the approximate capitalization rate for for buildings similar to yours (in size, desirability and condition of the property), in the same or similar neighborhood, you can use this formula:

How can I find out the capitalization rate in my neighborhood and how does that apply to me anyway?

Check residential income property listings in various real estate sales websites, such as loopnet, or look at commercial real estate brokers’ listings on their websites.. The listing will often show the capitalization rate which wil likely be between 3% to 5% in San Francisco, depending upon the neighborhood. Some listings will also base the value of a building based upon the gross rent multiplier (GRM). More on that in a moment.

Note that almost all buildings with less than five units will have a lower capitalization rate and are not strictly evaluated on capitalization rate because they are more desirable for condo conversion, TIC sales, etc., thus increasing their value.

Now let’s figure out the true value of tenant buyouts from the landlord’s prospective using one more calculation.

Here’s a fairly typical scenario: Tenant has lived in a two bedroom flat in a four unit building in the Lower Haight for ten years and a new landlord has just purchased the building. More often then not a new landlord will be the one offering the tenant a buyout. He’s an investor, a capitalist, an MBA bean counter who never considered starting a company to make something useful. He’s only in it for the money. He doesn’t care what happens to you.

The tenant is considering taking a buyout and wants to know how much it might be worth. Her rent is $2,000 per month and, after checking rents in the neighborhood, she thinks the landlord could charge $5,000 per month on the open market without much renovation. Her rent differential (market rate minus rent controlled rate) is $3,000 per month or $36,000 per year. This can be considered as net income because it is based on the fact that all the landlord needs to do is re-rent the unit at market rate. His expenses will be minimal. I always try to be conservative when I estimate the value of a buyout to the landlord, so I calculate the value based upon a 5% cap rate. $36,000 divided by 5% (36,000/.05). The value of the building will increase by $720,000 if the tenant accepts a buyout. The landlord (or his lawyer) will likely claim that he will have to remodel the unit to assure that he can rent it for $5,000 per month. Fine, even if he pays $100,000 to remodel, and at that price, it may include a gold plated toilet or two, the value of the building will increase by $620,000.

I took a quick look at a few residential income property listings in the Lower Haight. A conservative gross rental multiplier of about 12X might be appropriate here. I actually saw a few at 17X. The projected gross rent for the unit would be $5,000.00 per month or $60,000 per year. 12 X $60,000 = $720,000. Waddaya know?

Is my hypothetical client going to get half of the increased value in a buyout? Not likely. However, with more research she may be able to understand the landlord’s true breakpoint and increase her buyout accordingly. Most tenants simply don’t realize how much money they may be leaving on the table.

Tenant buyouts are only as good as the agreement that sets the terms.

In my article, Tenant Buyouts: The Agreement, I listed all of the terms that, I think, belong in a buyout agreement. Get half of your money up front in the agreement. Make your move-out date on the first of the month rather that the last day of the month. Don’t agree that the landlord will refund your security deposit “according to law.” Add a clause that allows you to leave the unit in “broom clean” condition. Releases in the agreement should always be mutual. Insist on an attorneys fees clause to a the prevailing party enforcing the agreement. All of these are still important today.

It’s still a game of chicken.

In my experience, landlords threaten eviction, but offer buyouts because they don’t really want deal with the ramifications of an eviction. An Ellis Act eviction would prevent the landlord from renting for five years and/or prevent condo conversion. Landlords may threaten to move in, but most really don’t want to live in the unit for the required three years. Remember, a buyout agreement will usually contain a release of all the tenant’s future claims—lucrative claims for wrongful eviction.

That’s why it is very important to gather all the facts you can to help you decide whether to take a buyout. Even then, some landlords will serve an Ellis Act eviction because it’s part of their business plan. Even then, some landlords will serve an OMI eviction because they either—can’t or won’t—pay enough to justify a tenant’s waiver of future rights.

If you are facing an Ellis or OMI eviction threat you should contact the Displaced Tenant Housing Preference Program prior to the landlord’s service of a notice to understand if the program is one that you can use, and more importantly, to assign a monetary value to the housing voucher that you can consider as part of your bottom line for negotiation.

If you have been served with an Ellis eviction notice, I recommend that you call the Tenderloin Housing Clinic to seek legal representation.

Taking a buyout will be one of the most difficult decisions you ever make, unless you plan to move in the near future anyway, or the money you get will complete the down payment you been saving.

Only you can decide whether to take a buyout.

Call the Tenant Lawyers now for a free consultation.

(415) 552-9060

My 24-Unit Building Is For Sale, Should I be Worried?

The impending sale of a building these days, even 24-unit building like yours, should concern tenants. An impending sale also provides them an opportunity to connect, organize and take power.

Should I Propose A Buyout to My Landlord?

Correctly or not, landlords figure that a tenant offering a buyout may be ready to move voluntarily anyway–as in already found a new place and wants some quick cash to exit.

Should I Take A $40,000 Buyout Offer?

I am 65 years old. I’ve lived in my apartment for 22 years. I pay just under $900 for a junior one bedroom on the top floor in the San Francisco Mission district.The landlord offered me a buyout to vacate for $40,000. Should I ask for $60,000?

Are The Buyout Terms My Landlord’s Offering Acceptable?

Should we sign the buyout agreement the landlords provided or renegotiate?

Tenant Buyouts: The Agreement

If you negotiated a buyout agreement with your landlord, get that agreement in writing. Any landlord who balks at this is going to screw you, end of story.

Tenant Buyouts: Strategy for Success

Like a high stakes poker game, buyouts are complicated. If you want want to get the best deal possible, you must be prepared to analyze the deal using the strategies here.

Tenant Buyouts: Your Absolute Bottom Line

If the landlord offers our tenant family a buyout of $20,000 to move they should politely tell him to gently insert his offer into a location devoid of sunshine.

Buyouts

If you negotiate a buyout with your landlord, you don’t want to be the tenant plummeting off the cliff. That is why we will help you if you decide to take a buyout.